Finance new or used continuous miners for underground coal and soft rock mining. $50k minimum, B/C credit considered, application-only to ~$400k, funding in about 1-2 weeks.

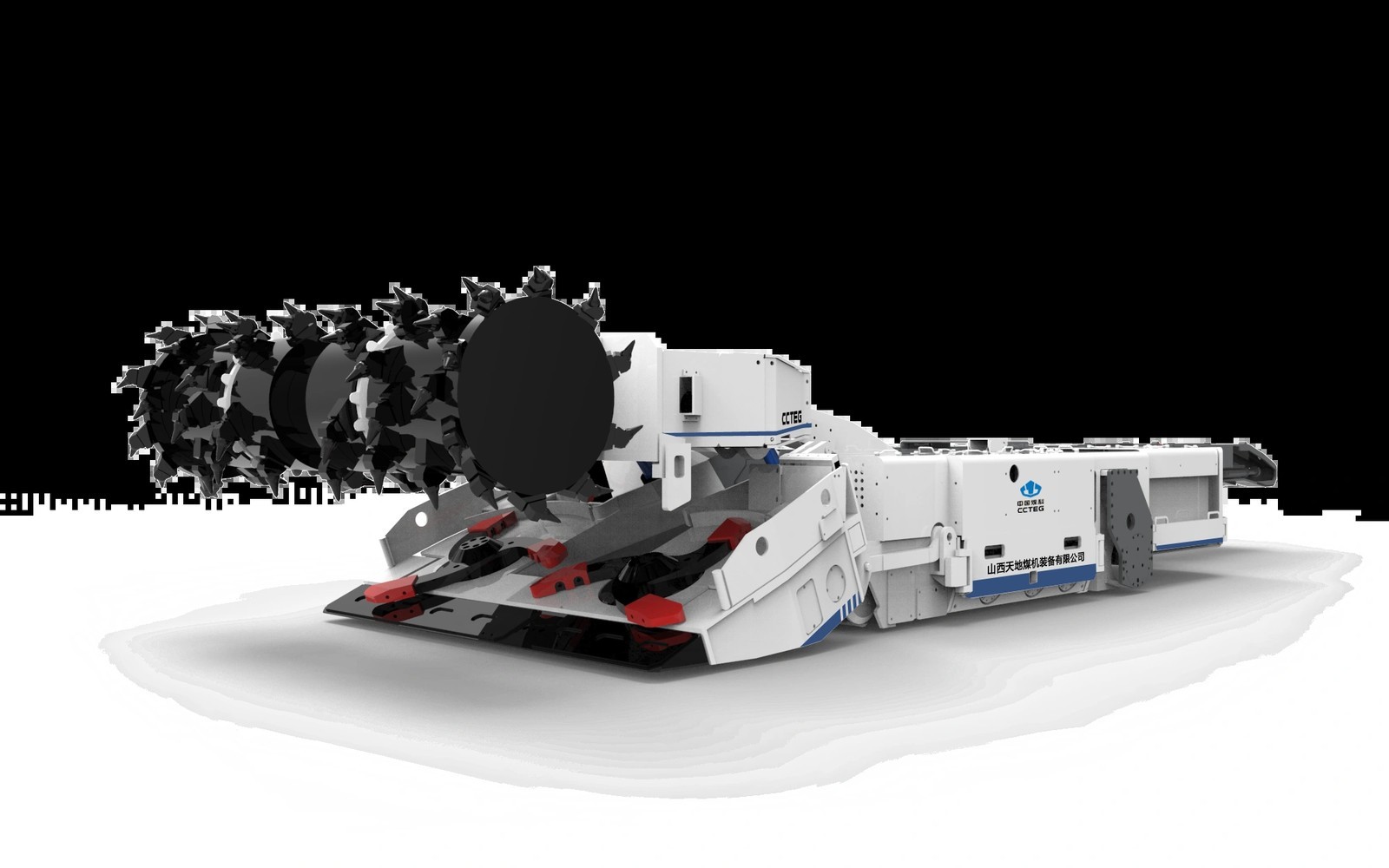

Continuous miner availability is the throughput equation in a room-and-pillar operation. When the machine is cutting, ore or coal is moving. When it is down, the section stops, the shuttle cars sit idle, and the production plan falls behind. We finance continuous miners for underground coal operations in Appalachia and the Illinois Basin, for trona mining in Wyoming's Green River Basin, and for other soft rock applications where the continuous miner is the primary extraction tool.

A new continuous miner from Joy (now Komatsu Mining) or Sandvik ranges from roughly $1.5 million to $3 million depending on the machine class, cutter head configuration, and tram horsepower. Used units that have been rebuilt or overhauled trade at substantial discounts but still require financing in the hundreds of thousands. We handle both ends of that market. Our minimum is $50,000, our sweet spot is $100,000 and above, and we consider B and C credit where the asset and operating context support the deal.

We structure continuous miner financing as equipment loans or finance leases with terms that match the equipment's productive life in your specific application. Application-only approval is available up to approximately $400,000. For larger machines and full rebuilds, we typically need three months of bank statements and supporting documentation on the equipment. Most funded deals close in about one to two weeks from completed application.

Continuous Miners: The Asset Behind the Credit

The two dominant continuous miner platforms in the U.S. market are the Joy series from Komatsu Mining and the Sandvik MB series. Earlier Joy machines, particularly the 14CM, 14LS, and 12CM series, remain in service at coal mines across eastern Kentucky, southern West Virginia, and southwestern Virginia. Sandvik's machines have a meaningful share in trona mining in Wyoming, where the formation's geology and chemistry make the continuous miner method the standard approach. Both brands have rebuilt and remanufactured programs that can extend machine life substantially.

What matters in underwriting a continuous miner is not just the model year but the rebuild history. A 2008-model Joy continuous miner with a full remanufacture done by the OEM or a certified rebuilder, including a new cutter head, new sumping cylinders, and rebuilt tram motors, is a fundamentally different credit than the same year machine running on original hours with deferred maintenance. We ask for rebuild documentation because it drives our term structure and advance rate decisions.

Cutter heads are where a lot of the wear concentrates and where a lot of replacement cost lives. In harder coal seams or abrasive formations, bit consumption is high and head rebuilds happen frequently. That maintenance cycle is a real cost and a real financing consideration. Continuous miners operating in Pocahontas or Sewell seam conditions in southern West Virginia face different wear economics than machines running in the softer coals of the Illinois Basin. That context matters when we structure the deal.

Trona miners working the Green River Formation inGreen River, WYandRock Springs, WYoften run machines in configurations specific to the trona seam geometry, including specialized cutter heads and dust suppression systems for the alkaline environment. We have financed equipment in this application and understand the production economics that trona operations actually run on.

New, Used, and Remanufactured Continuous Miners

New continuous miners give you warranty coverage, current safety systems, and OEM support. They also come at prices that require serious capital commitment. For a large underground coal operator adding a second section or replacing an end-of-life machine, new is often the right call and we can finance from dealer invoice.

Used continuous miners purchased through auctions, mine dispersals, or dealer trade-ins can represent real value. A machine that has been idle during a production curtailment and maintained through the downtime is very different from one that was worked hard and sold in distress. We finance used units and rely on condition reports, rebuild documentation, and in some cases third-party inspections to establish value and inform our structure.

Remanufactured machines from OEM programs or certified third-party rebuilders sit in a distinct category. These machines often carry limited warranties on the rebuilt components, and the documentation that comes with a proper remanufacture is exactly what we need to support a multi-year term.Used mining equipment financingcovers these acquisition types and the approach is the same regardless of whether you sourced the machine from an auction house or directly from the rebuilder.

Underground coal's capital cycle has been compressed over the past decade as some operators have deferred new machine purchases in favor of extending the life of existing fleets. That means there is a real market in rebuilt and extended continuous miners that makes up a significant share of what we finance. We do not treat a rebuilt 2012-model machine as inferior to a new machine on principle. We evaluate it on the actual rebuild scope and remaining productive life.

Who Uses This Financing

Contract mining companies operating room-and-pillar sections under production agreements with coal operators or mineral property owners. Your revenue is tied to tonnes mined, the equipment has to be in place before you can mine, and the machine has to be available when your contract says it should be. That timeline is real and we fund on it.

Underground coal producers adding sections or replacing aging equipment at existing mines. Operational cash flow in coal tends to track closely with production volume, and a new or rebuilt continuous miner that improves section advance rates translates directly into revenue. That logic informs how we think about the credit.

Trona and potash operators in the Powder River Basin and Green River area where continuous mining is the standard production method. We finance these operations as part of our broader coverage oftrona and potash mining equipment financing.

Operators pursuingcoal mining equipment financingacross Appalachian and Interior Basin operations who need a lender that does not flinch at underground coal credits. We do not avoid the sector. We underwrite it on the asset and the operation's actual economics.

Refinancing and Cash-Out Options on Continuous Miners

A continuous miner that is paid off or carries a low balance relative to its market value is an asset you can put to work in a second way. A sale-leaseback converts that equity to cash while keeping the machine at the face. We buy the miner, lease it back to you at a monthly payment that works with your production economics, and you access the capital. That cash has funded everything from section ventilation upgrades to new shuttle car acquisitions to working capital during a longwall move.

Refinancing an existing note is another option if your current rate or payment does not match where rates have moved or where your credit stands today. A company that financed a continuous miner three years ago under tighter credit conditions may qualify for a better structure now.Equipment refinancingis straightforward when the machine is well documented and still in active production. We pull the payoff, establish current value, and build a new structure that reduces your monthly obligation or pulls cash out.