Finance a complete mineral processing plant or individual circuit components from $50,000 up. Application-only to ~$400k, B/C credit considered, funding in about 1-2 weeks.

Tonnage through the mill is the number that matters. Everything upstream, from the drill pattern to the haul cycle, exists to feed a processing plant that converts broken ore into saleable product. A plant running below design capacity because capital is tied up in the wrong places is a plant bleeding margin on every shift. We finance mineral processing plants and individual circuit components for mining operations across coal, hard rock, industrial minerals, and aggregate, with deal sizes that range from small wash plant upgrades to multi-million dollar greenfield installations.

Processing plant financing covers a wide range of assets: primary and secondary crushers, SAG mills, ball mills, flotation cells, gravity concentrators, thickeners, filtration equipment, cyclone systems, and the structural and mechanical balance-of-plant that ties it all together. A complete plant can represent tens of millions in capital. Individual circuit additions, like a secondary cone crusher or a new flotation bank, often fall in the $500,000 to $3 million range where application-only approval may not cover the full amount but where a streamlined credit process still applies.

Our minimum transaction is $50,000 and our sweet spot runs from $100,000 into the millions for plant-level credits. We handle purchase, refinance, andsale-leaseback financingon both new installations and existing operating plants. B and C credit are considered where the asset and production history support the deal. Most funded transactions close in approximately one to two weeks.

What Lenders Need to Understand About Processing Plant Assets

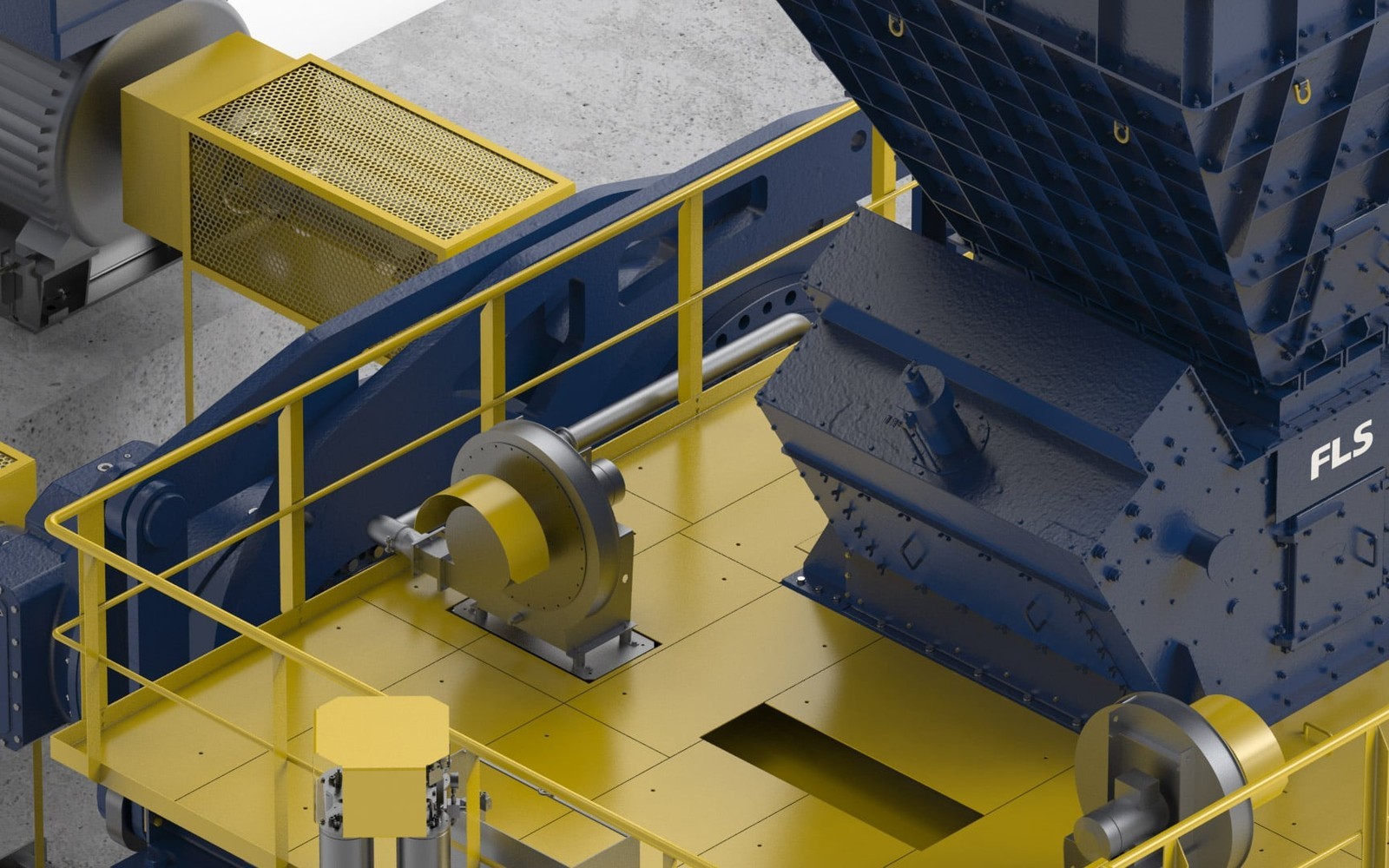

A mineral processing plant is not a single piece of equipment. It is a system of interdependent assets with highly variable salvage value, installation costs, and relocation economics. Lenders who do not understand this tend to either overprice the risk or refuse the category entirely. We have financed processing infrastructure for operations ranging from alluvial gold to copper porphyry, and the financing structure needs to match the asset's characteristics.

Fixed installations are the most common case. A ball mill anchored to a concrete foundation with a dedicated drive system is not going anywhere. That permanence works in your favor in some credit conversations and complicates collateral positions in others. We are experienced at working through lien and fixture filing questions that trip up general lenders.

Modular and skid-mounted plants present differently. A containerized gold processing plant or a portable wash plant on tracks has real mobility value. If a project does not perform, the equipment can be relocated to the next site. That optionality improves recovery assumptions and can result in better advance rates or longer terms compared to fixed infrastructure of equivalent dollar value.

Used and refurbished processing equipment from mine closures or project suspensions represents a significant portion of the market. A flotation circuit from a closed copper mine, recommissioned for a new project, may deliver most of the performance of new equipment at a fraction of the capital cost. We finance these acquisitions and work with refurbishment contractors on progress-draw structures where appropriate.Used mining equipment financingapplies here, and we understand the documentation that comes with surplus asset acquisitions.

How Plant Financing Is Structured

Processing plant credits are typically structured as equipment loans or finance leases with terms ranging from three to seven years depending on asset type, age, and borrower profile. A new SAG mill from a recognized OEM on a ten-year mine life supports a longer term than a fifteen-year-old flotation circuit being refurbished for a junior miner's first project.

We usually finance the equipment cost directly. Civil and installation costs are sometimes bundled when the civil work is contracted separately and documented clearly, but we underwrite against the equipment value. That distinction matters because the processing equipment itself has identifiable market value; poured concrete does not.

Where a plant acquisition is complex, we sometimes structure progress draws against confirmed delivery and installation milestones. This keeps capital moving in step with project completion rather than requiring the buyer to front all costs and refinance at the end. For operations looking atmining equipment loansversus leasing structures, we walk through the tax and balance sheet differences so you pick the structure that actually fits your situation.

Sale-leaseback on existing processing infrastructure can free up capital without disrupting operations. An operating plant that is paid off or partially paid represents real equity. We buy the plant, lease it back to you, and you deploy the capital elsewhere in the business. That structure has funded exploration programs, tailings management projects, and working capital buffers for operations awaiting payment under offtake agreements.

Processing Plant Capital in Current Mining Markets

Critical minerals policy, battery supply chains, and sustained demand for copper have pushed a wave of new processing capacity into development. Projects that sat on the shelf for years because commodity prices did not justify capital expenditure are now moving. That is creating real demand for processing plant financing outside the traditional project finance window that large mines use.

Junior miners, contract processors, and merchant tolling operations often cannot access bond markets or large bank syndicates. Their capital needs fall between what a commercial bank will touch and what equipment rental addresses. That is exactly the space we work in. If you are financing a small to mid-scale processing plant for a copper, lithium, or rare earth project, you are the borrower we understand best.

Aggregate and industrial minerals processing has its own capital cycle, driven more by construction activity and regional demand than commodity prices. A crushed stone plant or a silica processing facility has a different credit story than a precious metals circuit, but the financing mechanics are similar. We handle both and do not require clients to translate their business into mining-specific language before we can help. For operations focused on specific minerals, ourcopper mining equipment financingandlithium mining equipment financingpages carry more detail on what those sectors look like in practice.

Credit and Documentation for Processing Plant Deals

We underwrite plant financing on the combined picture of the borrower's credit, the asset's value and condition, and the production context. No single factor is disqualifying on its own. A strong asset and a clear revenue story can carry a credit profile that a conventional lender would decline. A strong balance sheet can support a deal where the asset is older than a bank would prefer.

For transactions up to roughly $400,000, application-only approval is available and we do not require full financial statements. Above that threshold we typically want three months of bank statements at minimum, and for larger plant-level credits we may want profit-and-loss statements or prior year tax returns to see the production and revenue picture. Equipment invoices, appraisals, or auction sale documents establish the asset value. For used or refurbished plants, a condition report from a qualified inspector is helpful and sometimes required.

B and C credit situations are handled on a case-by-case basis. A mining company that went through a contract gap, a commodity price downturn, or a project delay that affected credit is a different risk than a company with no clear path to revenue. Context matters. We look at where you are now, not just where the score has been. Thebad credit equipment financingpage covers how we think about that in more detail.