Finance a mobile crusher for aggregate, mining, or construction recycling. $50k minimum, application-only to ~$400k, funded in 1-2 weeks. New and used.

A mobile crusher's production number only counts when the machine is in front of the material. Availability matters here just as much as it does in a fixed plant, and for operations that depend on moving the crusher to successive faces, pits, or job sites, the duty cycle has to hold across the relocations as well as the crushing hours. We finance mobile crushers for quarry producers, contract crushing contractors, recycling operators, and mine development teams who need primary or secondary reduction capacity that can follow the work.

Our minimum transaction is $50,000, and mobile crusher deals commonly run from $100,000 for compact secondary units to $500,000 and above for large track-mounted primary configurations equipped with on-board screening and conveying. Application-only decisions are available up to approximately $400,000, and most applicants in that range receive a credit determination within 48 to 72 hours. Full underwrite files for larger transactions typically close in one to two weeks with three months of bank statements and basic business documentation.

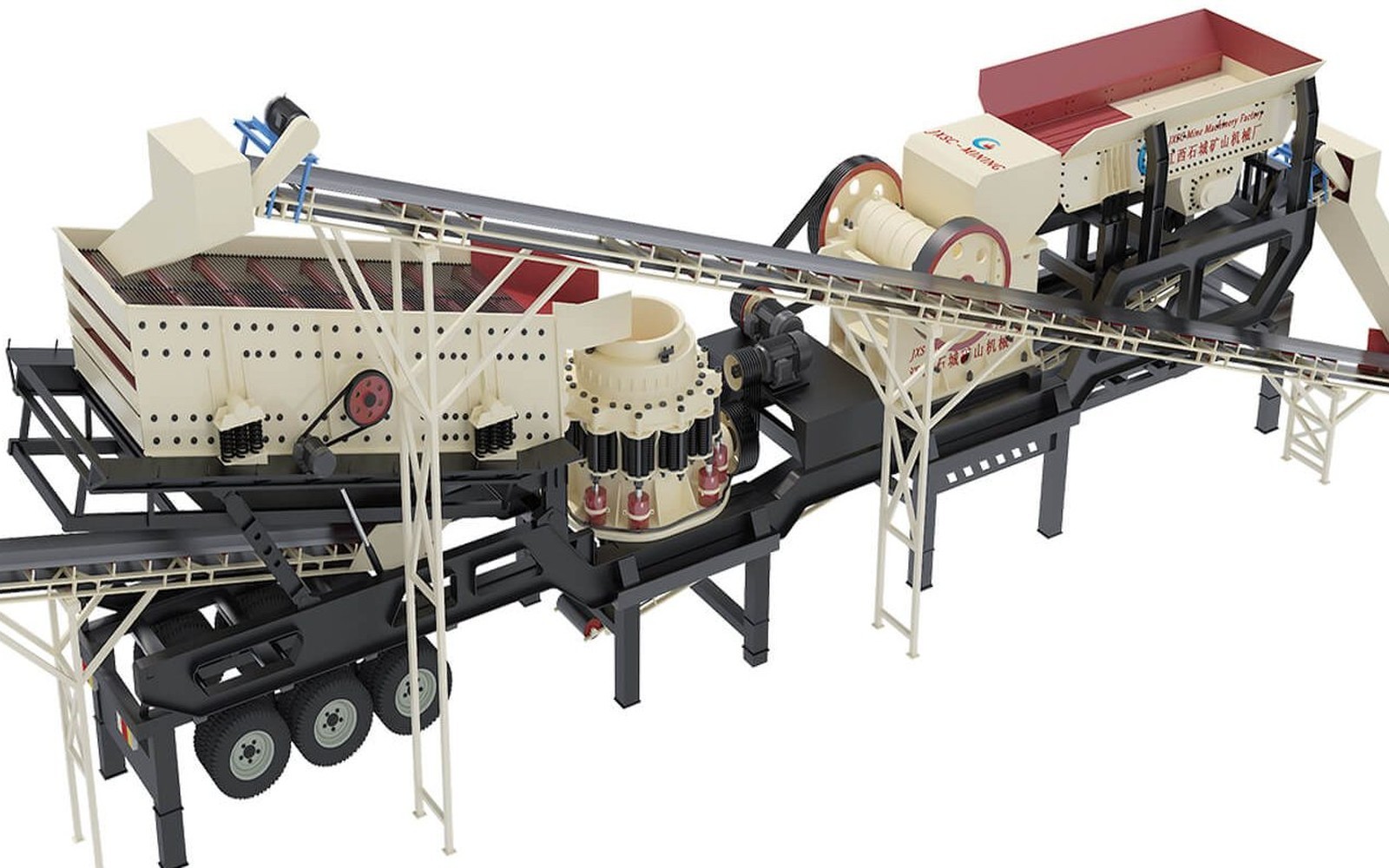

Mobile Crusher Types and What Determines Their Value

Mobile crushers span three primary configurations by crushing mechanism: mobile jaw crushers for primary reduction of hard, abrasive feed material; mobile cone crushers for secondary and tertiary reduction producing cubical aggregate; and mobile impact crushers suited to softer limestone, concrete recycling, and demolition debris. Each type carries distinct residual value characteristics that affect how lenders approach the asset.

Jaw-based mobile crushers tend to hold value well across a broad range of feed materials and are the most versatile collateral in this category. Track-mounted self-propelled units typically command better financing terms than wheel-mounted tow-behind versions, because the track machine can move independently, has broader market appeal, and represents a more complete production unit. Engine hours and crusher hours are both tracked separately on most modern machines, and the relationship between the two tells a lender a great deal about duty cycle intensity.

Brands financed regularly in this space includeMetso Lokotrack, Kleemann,Terex Finlay, McCloskey, and Keestrack units, along with older generation machines from Sandvik and Extec. We assess used units based on current engine and crusher hours against the OEM rebuild interval, the condition of the wear surfaces (jaw plates, mantles, blow bars, or impact bars depending on type), and the availability of service records.

Where Mobile Crushers Work in Mining and Aggregate

In the aggregate sector, mobile crushers are a core production tool for quarry operators running multiple pits, contractors producing spec material for DOT projects, and recyclers processing concrete and asphalt for base material. The economics are clear: a mobile plant eliminates the haul from face to fixed plant, reducing transport costs and allowing production to happen closer to the work face as the quarry advances.

In mining, mobile crushers appear in bulk sampling programs, in development crushing during pre-production phases, and in in-pit crushing and conveying (IPCC) systems where primary reduction happens inside the pit to reduce haul truck tonnage to the surface. Operations focused onsand and gravel,crushed stone, andcontract miningare frequent users of mobile crushing equipment, and we see transactions from all three segments regularly.

The recycling and construction demolition sector runs a parallel market for mobile impact crushers that process concrete, brick, and asphalt into recycled aggregate. These operators often work project-to-project, and the credit situation looks more like a construction contractor than a mining company. We finance both profiles.

Refinance and Sale-Leaseback Options

Operators who own mobile crushers outright or carry an existing loan with equity built up have two tools available beyond a new-purchase transaction. Cash-out refinancing allows an operator to place a new loan against an owned or partially-paid-down machine, receiving the difference between the new loan amount and any payoff as cash in hand. This works for operations that need working capital, want to fund a second machine, or are covering mobilization costs on a large contract.

Sale-leasebackis a cleaner version of the same concept: the machine is sold to the lender and simultaneously leased back to the operator at a payment that reflects the agreed value. The operator continues using the machine without interruption, and the cash proceeds come in at closing. For crushers that have appreciated in a strong used-equipment market, the sale-leaseback price may exceed the book value significantly. We value the asset based on current condition and market comparables, not the original purchase price.

Operators with existing financing on a mobile crusher can also exploreequipment refinancingto lower a payment, extend a term, or restructure around a changed cash flow situation. We can pay off the existing lender and re-write the deal under current terms.

How Quickly This Moves

Speed matters when a machine is available at a dealer or through a private seller and other buyers are in line. Application-only transactions under approximately $400,000 can receive a preliminary decision in one to three business days. Once approved, funding is typically ready within one to two weeks. Private seller transactions add a step for lien search and title review but generally do not add more than a few days to the timeline.

For contractors who are actively bidding work and need financing in place before committing to a machine purchase, we can issue a pre-approval letter that specifies the amount and structure we are prepared to fund. That letter gives you credibility with a seller and keeps the negotiation moving without waiting for a full underwrite to complete every time a machine becomes available.